Do I Need a Credit Card?

Do you really need a credit card? Everyone seems to have at least one and it seems like a useful financial tool for purchases, right?

But according to the Money Mate site, the overall household debt in Singapore reached S$371.39 billion in July 2021. That’s an increase of over 10% from the previous year!

Financial distress and spending beyond one’s means could be the main causes of this.

So to understand the responsibilities that come with being a credit card owner and user, let’s take a look at some questions you must ask yourself first.

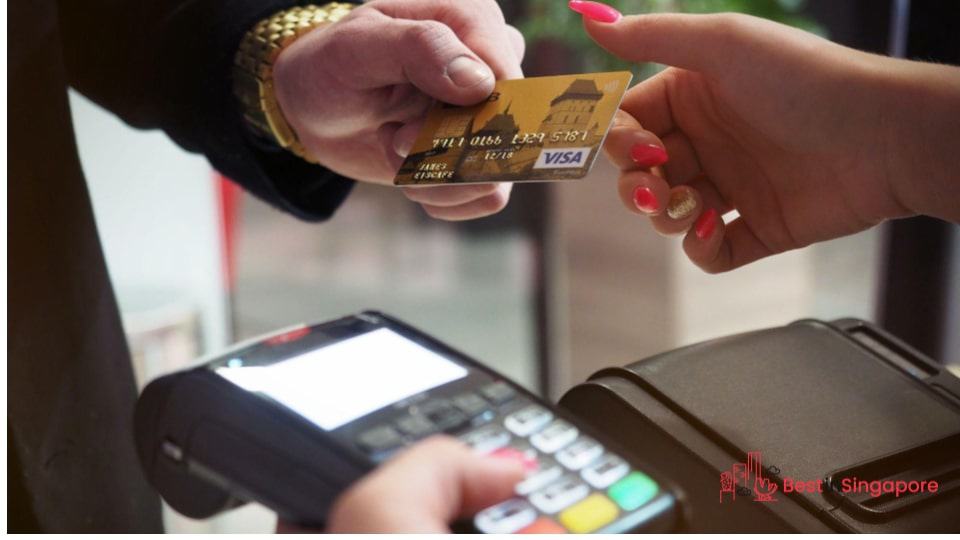

What’s your primary use for a credit card?

Do you like shopping (online or in physical stores) and using your credit card to pay for purchases? Or do you pay with your credit card for petrol on a regular basis?

It’s quite tempting to indulge yourself in the latest sales for clothes, gadgets, and other seeming “must-haves” that can be yours with a swipe (or a few taps) of your card. But bear in mind that using a credit card is basically like having a personal loan that you’ll eventually need to pay back.

So while it might be tempting to go down the cashless route to pay for things, it might be better to check how much you have in your savings account first. That way, you’ll know if you actually have the money to afford the things you’re looking to buy.

Do you want to earn rewards?

The best credit cards in Singapore offer a menu of benefits for their clients, including rewards and sign-up bonuses.

These rewards can help you pay for things like travel expenses and other purchases via cashback, miles, and cash bonuses. Corporate credit cards often operate with robust rewards systems due to businesses regularly covering employees’ plane tickets, hotel stays, and other expenses.

But you’ll need to go through the rewards rules and understand how much and how often, when, and where you’ll need to use your credit card to make the rewards worth your while.

And it’s equally important to be able to pay your full balance plus annual fees every month. It’s quite tempting to build up a huge balance just to earn rewards, but this is how credit card debts start.

Do you need it to save money while shopping?

The most prestigious credit cards in Singapore promise benefits and perks that only the truly wealthy and privileged deserve (and can afford). But these cards also come with tens of thousands of dollars in annual and initiation fees which, to be honest, not a lot of us can afford.

Shopping malls like offering consumers tempting discounts or plans to make them purchase something on impulse. But unless you’ve made it a habit to pay your balance in full every month, you might actually be spending more on interests compared to the discount you thought you were so lucky to get.

So if the concern is to be able to save money on shopping, you might be better off using a debit card instead. You’ll be paying only for things you can actually afford with money you actually have while enjoying the convenience of a cashless transaction.

Are you going to use it for emergencies?

There’s a practical reason why health insurance in Singapore exists. It’s to help protect both your physical and financial health in case accidents happen and your health is compromised.

It’s also why you should consider getting personal accident insurance so you’re covered for most emergencies, especially if yours is a high-risk occupation.

But to use a credit card as your primary emergency fund is not advisable. Medical bills and other emergency-related services can be quite expensive and will quickly pile up if you aren’t careful.

You don’t want the mountain of debt that comes with using a credit card for emergencies. It’s better to build up a fund for it slowly but surely.